The consistent decline in inflation reading and Jerome Powell's recent indication that the Federal Reserve may consider cutting rates in 2024 have led to an increased sentiment that the economic slowdown anticipated in the U.S. in 2024 may be a "soft landing" rather than a true economic recession.

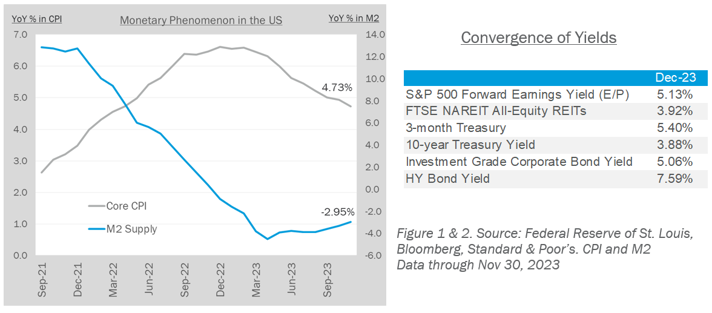

The restrictive monetary policies of the Federal Reserve over the last two years have helped taper the year-over-year growth in the supply of money (M2) in the economy. With a lag, we have seen year-over-year inflation come down to 4.7% at the end of November 2023. While not at the target 2% inflation rate, Powell indicated that the Central bank was aware of the risk of keeping rates at restrictive levels for too long. Given the dynamics of rising rates over the last two years, we have noticed a convergence in yield across equity and fixed-income instruments. Income-generating instruments, from REITs to corporate bonds, compete with cash equivalent yields. When clients meet near-term liquidity needs, it is easier to raise the cash in anticipation of the cash need even a few months out, as they are paid to hold cash and not take market risks.

Despite concerns over higher borrowing costs, higher input costs, and restrictive U.S. fiscal policies, the U.S. economy grew at an impressive rate of 4.9% in the third quarter of 2023 while inflation continued to trend lower. Consumers have remained resilient, supported by a tight labor market, but delinquencies have picked up for credit card and auto loans. Corporations that secured long-term fixed-rate borrowing before 2022 fared well, but areas such as commercial real estate, which rely on floating-rate borrowing costs, have seen their net operating income decline as short rates increase.

The major Global equity and fixed-income markets recouped much of the losses they incurred in 2022, with some exceptions, notably China. Much of the gains came through in the second half of 2023. This may be in anticipation of falling rates in 2024, which will likely happen in tandem with an economic slowdown. As we explain further in this letter, there is considerable dispersion in performance across the underlying constituents within each market.

While near-term performance is always hard to predict, the volatility will likely remain high in both equity and fixed-income markets.

Access the Canterbury Outsourced CIO: Fourth Quarter 2023 Commentary