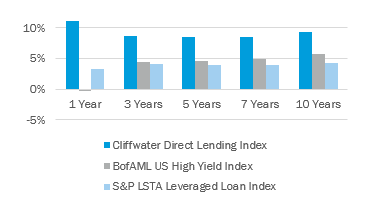

In 2018, Canterbury formed an internal environmental, social, and governance (ESG) committee to synthesize and streamline the ever-growing ESG investment universe. The committee has since created a framework and toolkit to assist clients in finding customized ESG solutions that align with their mission, values, or investment process. Canterbury defines ESG as three separate categories: exclusionary screening, best-in-class selection, and positive impact.

In this first part of our three-part series on ESG, we will focus on exclusionary screening and how it can be implemented across client portfolios.

In the broadest sense, exclusionary screening removes companies and/or sectors from an investment portfolio that contradict a client’s social or moral values. Exclusionary screening and responsible investing gained prominence during the 1960’s and 1970’s when investment products were created to address political and social issues of the time. The application of responsible investing was originally implemented through the exclusion of certain companies (i.e. divestment) or through shareholder activism — where proxy voting and discussions with large stakeholders regarding environmental, social, or governance issues led to targeted change within a company. Thematic investment strategies emerged that also excluded companies who violated key issues of the time. Key ESG issues have evolved, but values-based considerations have always been wide-ranging and span across E, S, and G. Some of the current issues are listed below:

While responsible investing and large-scale issues are debated and discussed today with organizations, such as the United Nations-supported Principles for Responsible Investment (UN PRI), investors have more tools and resources than ever to target values that matter specifically to them. Canterbury believes that clients should have the choice to incorporate their mission and values in their investment portfolio. Exclusionary screening can be used as one of several methods to reach a specific ESG outcome.

A number of Canterbury clients have implemented exclusionary screening practices within their investment portfolios for several years. Canterbury has assisted clients in screening equity holdings in both passive and active strategies by using MSCI ESG Manager’s Business Involvement Screening Research. This program is an online product that provides data feed that can be used to research and screen securities on the basis of criteria that can be specified per a client’s investment guidelines.

Screening criteria based on business involvement can be measured as follows:

The following is a sample illustration of the screening process. The table lists a number of criteria that have been defined for screening a portfolio of equity holdings.

Exhibit A. Source: MSCI

Using MSCI ESG Manager, we can also produce a report on the individual companies within a custom portfolio or passive benchmark with each company’s ESG ratings. A sample of this report is shown below.

Exhibit B. Source: MSCI

The investor can then determine whether to exclude a flagged company in their separately managed account. However, portfolio construction and risk/return considerations must factor into the analysis.

Excluding companies from investment strategies or across an entire portfolio can have significant implications on return, risk, and portfolio construction. For example, screening out companies within concentrated strategies can meaningfully change the investment style or mandate and constrict the manager’s opportunity set and ability to outperform the benchmark. Heavy screening can also lead to unwanted concentration exposure, and specific industries or factors may be unintentionally expressed based on an ESG screen. Investors should tread carefully when applying screens to actively invested strategies and engage in an open dialogue with their investment managers.

Investment managers that optimize passively managed portfolios to align with one’s values without taking on undue risk have expanded and grown more sophisticated over the last several years. Canterbury partners with firms that utilize quantitative systems to adequately screen out unwanted companies or sectors and also maintain comparable risk/return profiles relative to the traditional passive exposure. Taken one step further, investors can incorporate ESG ratings and integrate forward-looking ESG factors into the portfolio. As such, investors are able to incorporate their values from either an exclusionary or inclusionary perspective. We will investigate ESG integration, otherwise known as best-in-class selection, in Part II of our ESG Series.