When a corporation earns a profit or surplus, it can pay a portion of that profit as a payment to shareholders in the form of dividends. This is how companies have distributed profits to shareholders for centuries. In the early 1600s, the Dutch East India Company was the first recorded public company ever to pay regular dividends. It went on to do so for nearly 200 years.

Today, companies have another option in their arsenal to distribute wealth to shareholders. The most common form in the United States is share buybacks (or share repurchases). This is when a corporation repurchases a portion of its shares in the open market.

This blog post examines the use and benefits of dividends and share buybacks in the United States and Europe, as well as the significant impact of COVID-19 on these forms of profit distribution. Furthermore, we compare the shareholder yield metric, which is a more complete measure of shareholder return, to the dividend yield metric.

According to Bloomberg as of September 1, 2020, 76% of the S&P 500 companies pay a dividend in the U.S. However, just 189 of those companies pay out more than 50% of earnings.1 The dividend payment to earnings ratio, commonly known as the payout ratio, has seen a steady decline in the U.S. since the end of World War II. By the late 1990s, share repurchases became the preferred method of profit distribution in the U.S. Amidst the current coronavirus pandemic, U.S. companies have benefitted from the lower payout ratio in the form of dividends and the flexibility of share repurchases.

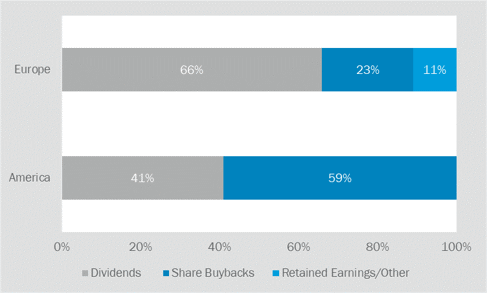

By contrast, European corporations distributed 66% of profits on average as dividends and only 23% as share buybacks in 2019, according to The Economist1. As a result, the larger portion of profit distribution in the form of dividends has led to significant dividend cuts in Europe in 2020 relative to the U.S.

Dividends vs. Share Buybacks in 2019

Exhibit A. Source: The Economist1

In recent months, companies across the globe including many blue-chip companies such as Royal Dutch Shell, BP, Barclays, Ford, Boeing, and HSBC have experienced headwinds due to the COVID-19 pandemic. These companies have either significantly cut or completely halted dividend payouts.

Fortunately, not all sectors and regions of the market suffered the same fate. For instance, North American companies in Canada and the U.S. have been relatively resilient in the face of the pandemic. According to the Janus Henderson Global Dividend Index (JHGDI), only one in ten companies reduced or suspended dividend payouts.2 Furthermore, the total payouts in the second quarter of 2020 ticked up slightly versus the second quarter of 2019.

European ex UK dividends, on the other hand, have taken quite a hit, the paper further details. Fifty-four percent of companies reduced their payouts, of which two-thirds canceled outright. Relative to the second quarter of 2019, total payouts fell 45%. From a sector perspective, financials, consumer discretionary, and industrials were the most vulnerable.

JHGDI Total Dividends by Industry

Exhibit B. Source: Janus Henderson Investors as of June 30, 2020

As mentioned above, U.S. companies pay out much less on average compared to the EU as dividends. Instead, they make the majority of their distributions in the form of share repurchases. To conserve cash, companies have been able to maintain their dividend while dialing down repurchases. From March to July of 2020, around one-fifth of companies in the S&P 500 put repurchase programs on hold.

However, not all firms pushed the pause button. Some companies saw the economy faltering as an opportunity to buy back their shares that sold off. As an example, Berkshire Hathaway repurchased $5.1 billion worth of their stock in the second quarter, the most ever bought back by Warren Buffet and his team.

Share repurchases have been beneficial not only for management teams but also for shareholders. Buybacks reduce the total number of a company’s shares outstanding and tend to boost share prices. The shareholder has the flexibility to sell the stock, or to defer capital gains and taxes to a later period.

There are, however, concerns to share repurchases. Reduced shares in the open market can artificially boost earnings. For many executives, earnings metrics dictate part of their compensation. So, rather than focusing on the long-term value of a company, executives may instead be focusing on the short-term benefits of repurchasing shares.

For investors, it is often common to focus on dividends as the primary source of yield (or return). A more appropriate and robust measure, particularly for U.S. companies, is shareholder yield. This metric captures the three ways in which a public company distributes cash to shareholders: share repurchases, cash dividends, and debt reduction.

To illustrate, Apple at the end of August had a dividend yield of 0.62%. The shareholder yield for the tech giant was 6%. An investor focused on dividends may overlook the significant profit distributions through share repurchases. Moreover, the dividend yield measure reflects only a portion of investor return whereas the shareholder yield presents a more complete measure of distributions.

Many companies have faced significant headwinds in recent months. As countries reopen, companies can get back to business and start to reimplement payouts in the coming quarters. To help support the economic recovery, the Federal Reserve announced at the end of August 2020 that it plans to keep rates near zero even after inflation exceeds its target level. In the current low rate environment, with real rates close to or near negative, stocks offer relatively attractive shareholder yields. As of third quarter-end, the S&P 500 shareholder yield was 4.2% according to JPMorgan while the 10-year Treasury yield was 0.65%.

In the 1980s, share repurchases were less common, and thus dividend yields during that time were similar to the shareholder yields we see today. In other words, it appears profit distributions have not significantly changed, but the ways shareholders receive the profits have. Just as companies have shifted the ways they distribute cash to shareholders, so too can investors shift the way they view yield.

Sources:

Bortz, Jason and Anderson, Reagan. CARES Act: What investors and small businesses need to know. (Capital Group, accessed Oct. 7, 2020.)

The CARES Act Works for All Americans. (U.S. Department of the Treasury, accessed Oct. 7, 2020.)

Public Charities. (Internal Revenue Service, accessed Oct. 7, 2020.)

Sources:

1 Big Tech is the new dividend royalty. (The Economist, Aug. 15, 2020.)

2 Janus Henderson Global Dividend Index. (Janus Henderson Investors, August 2020 edition.)